Common sense suggests this will precipitate volatile and unpredictable outcomes. As consumers and governments are pressured into more cautious behaviour than has prevailed in the past decade, investors should think about similar behavioural change.

Market review

While not quite having the drama of Joker versus Batman, the inflationary forces which are meeting highly indebted consumers and governments across the western world are creating a decidedly discomforting environment. The sources of inflationary pressure are many and varied. Profligate government spending and ultra-low interest rates during COVID, as well as supply chain interruptions and immigration shutdowns, no doubt contributed, and hopes of a rapid reversion as supply chain pressures eased have proven optimistic.

These pressures are hitting highly sensitive economies without much shock-absorbing capacity remaining, meaning policymakers are walking an uncomfortable tightrope. While the review of operations and performance at the RBA may be warranted, given central banks have undoubtedly been instrumental in fuelling asset price speculation and excessive borrowing, when it comes to tipping money into the real, rather than financial economy, governments probably need to shoulder more of the blame.

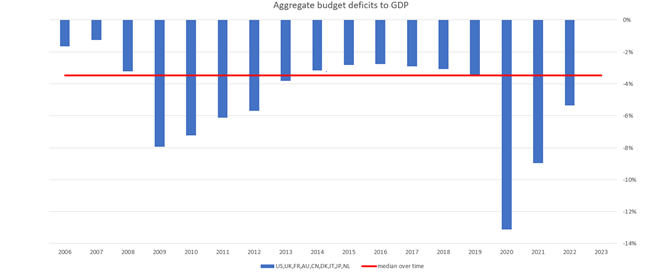

Looking at the financial system through a sustainability lens does not make for pleasant viewing. Cursory observation of the budget deficit position of major western economies suggests it has been some time since tax receipts bore much resemblance to spending, even ignoring the COVID-induced spike. Deteriorating demographics and a global inability to address issues such as spiralling healthcare and social security costs mean one needs to be an unbridled optimist to believe governments will ever be in a position to repay debt. Access to ever larger amounts of funding remains crucial as new deficits are added to the stock of debt requiring refinancing.

Given this picture, the term ‘risk-free rate’, the traditional benchmark against which other asset pricing is measured, may come under greater scrutiny in the future. Much of this has been the case for many years, meaning there is every possibility it may continue, however, in the famous words of Herb Stein, “If something cannot go on forever, it will stop”. Investing without countenancing the possibility of a change in these conditions is unwise and the direction of change is asymmetric.

Please note that mentions of securities, sectors and regions are for illustrative purposes only and not to be construed as an investment recommendation.

Source: Datastream

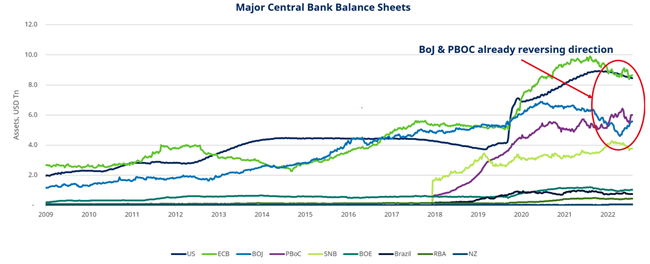

We have emphasised previously the importance of central bank intervention in supporting asset prices over the past decade. Much as we would prefer company-specific factors to be the primary driver of markets, evidence suggests otherwise. The correlation of equity market performance with central bank balance sheet size is alarmingly high. While savage moves in bond market pricing have occurred against a backdrop of minimal reduction in balance sheet size, incremental direction has been important. Price distortion is often gradual when natural buyers are crowded out; when artificial buyers leave and natural buyers return, wide price gaps can close abruptly. As is the case in equity markets (where turnover is declining) and property markets (where listings are declining), as increasing proportions of asset value sit in the hands of passive holders, fewer transactions are validating the valuations of an ever larger base.

Open marketplaces have been the most reliable way to determine fair prices for centuries. Any move away from this price-setting mechanism should be viewed with scepticism. Interestingly, recent months have seen major players such as the People’s Bank of China and Bank of Japan reverse direction. Rhetoric that suggested an appetite for shrinking balance sheets seems to have faded quickly as the prospect of anything resembling symmetry in asset prices proves scarier in practice than in theory.

Hit with a blunt instrument

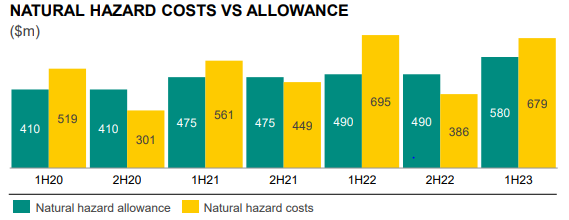

It never rains

Source: Suncorp Half-year Results Presentation

‘Future facing metals’ and the butterfly effect

When you leave marketing in the hands of miners you can’t expect miracles. Slogans aside, there is little doubt the sustainability debate has taken a more pragmatic turn in recent times. The insanity of adding up the carbon emissions in a portfolio is giving way to a recognition that new electricity grids, wind farms and environmentally friendly buildings will not be constructed from air and massively distorting capital provision to the economy will hinder rather than assist decarbonisation. The necessary materials will require incremental investment and even dramatically unpopular fossil fuel businesses require investment to sustain them while alternatives are constructed.

The enormous disparity in commodity pricing versus cost curves continues to present outsized valuation challenges, with sharp falls in spodumene and lithium pricing over recent months highlighting the risks in elevated pricing. While producers such as Pilbara Minerals have done an exceptional job of turning the price explosion into cash, the truth is no-one can profess great insight into price trajectory when governments, regulation and emotion create demand imbalances with which physical markets cannot keep pace.

The ‘butterfly effect’ potential from decisions that often reflect political expedience was starkly illustrated by the recent announcement from the Pakistan government that they were expanding coal-fired power generation from a little over 2GW to 10GW. As Europe managed to largely avoid the potentially disastrous outcome of energy shortages in a cold winter through commandeering every available LNG cargo at stratospherically high prices (the equivalent of US$400 per barrel oil), the butterfly effects were perhaps ignored. Across oceans, those energy shortages were inflicted on others. Pakistan, having invested in dominantly gas-fired power, and unable to compete with Europeans on price, wore the pain. Unsurprisingly, the victims sought to improve their own energy security through more diverse and reliable sources of energy supply. There seems little recognition that starving investment in gas production within Europe and sacrificed resilience and baseload capacity played a major part in initiating this sequence of events. We remain extremely wary of climate objectives that outstrip the ability of physical markets to keep pace. Engineering may need to trump politics, not the reverse.

Market outlook

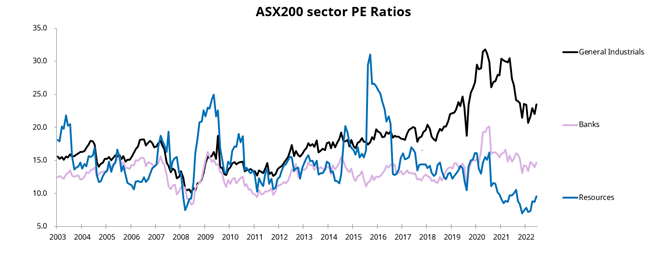

Beware of averages

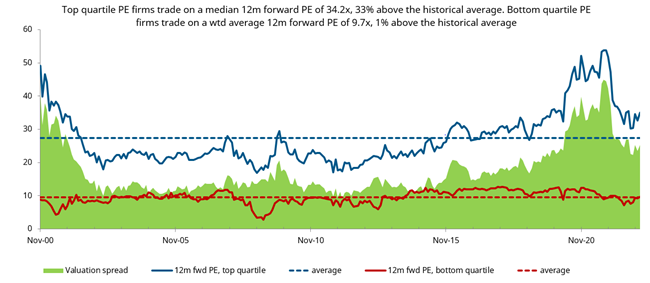

Distilling large amounts of data is tough. Average mortgage size, average age, average income, average household size; while countless measures such as these can provide insight into the health of banks’ balance sheets, demographic shifts, housing affordability, housing shortages and the economy more broadly, they can also disguise the picture. Average multiples in the domestic equity market are currently flattered by very low multiples for resource stocks and moderate multiples for banks. These are in turn supported by ongoing buoyancy in iron ore, coal, oil and lithium pricing in the case of resources, and solid net interest margins and virtually zero bad debt experience for banks. Industrial multiples remain elevated, and while a subset of industrial businesses are still enduring depressed conditions, many others are facing much tougher conditions. Characterising markets as reasonably valued based on averages is misleading. We would suggest markets are fairly fully priced when more sustainable earnings levels are incorporated.

Source: Factset, Schroders. Past performance is not a reliable indicator of future performance and may not repeat. For illustrative purposes and not an investment recommendation.

Asset prices and overconfidence